|

|

|

|

| Should I sell or keep my rental house?

|

|

|

|

|

The residents at my rental property in Tempe, Arizona gave notice that they will not renew their lease when it expires at the end of July. Should I attempt to find a new tenant or sell the house?

|

|

|

|

|

I originally purchased this home as a short term rental in 2022 when interest rates were cheap and Airbnb was booming. I put in new flooring, countertops, lighting, and invested in the landscaping to make it shine. The property performed okay as a short term rental in year one but after weighing the extra management cost, maintenance headaches, and high fixed expenses associated with a short term rental I decided to convert the home into a furnished long term student rental. That decision paid off. Since then the home has been rented for $3,500 - $3,600 per month with very little vacancy for the last three years.

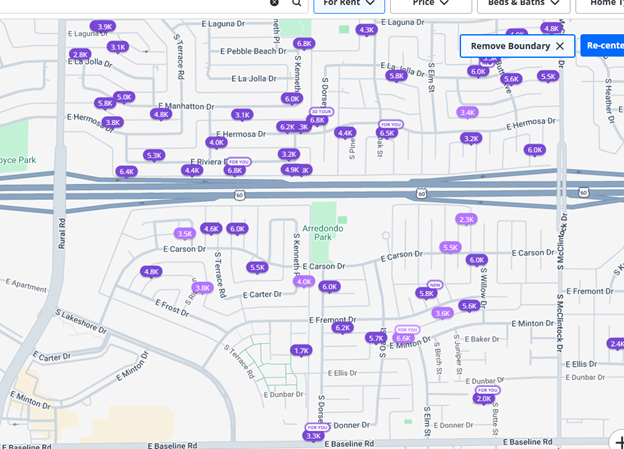

However, the market is changing again. Arizona was a hot spot for short term rental investment because of it’s friendly regulatory environment for short term rental operators. Many investors snapped up houses, renovated, and put them up on Airbnb. However, the glut of supply crashed short term rental prices and a lot of those operators are now converting to long term rentals. The increase in long term rental supply is causing some softness in the long term rental market. Check out the map below of houses for rent right now on Zillow just in the small area surrounding my house. Wow that’s a lot of single family rental supply!

|

|

|

|

|

Single family homes currently for rent in my neighborhood

|

|

|

The good news is all of the listings are above $3,000 per month and many are above $5,000 per month. My house is nicely updated but at just 1,340 square feet is one of the smaller homes on the market. I believe I can get the house rented for $3,640 monthly rent. When I bought the house in 2022 I thought the long term rent would be $2,600 per month. Single family rents have skyrocketed!

|

|

|

|

|

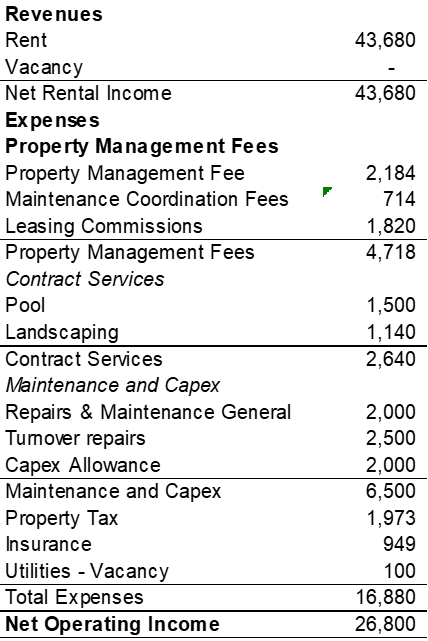

Below is my projected annual income assuming $3,640 rent with tenants paying for all utilities. Because it’s a student rental for Arizona State University students, I’m estimating 0% vacancy but an annual turnover with costs of $2,500 for turnover repairs (re-paint, miscellaneous repairs) and an annual leasing commission of 50% of the rent.

|

|

|

|

|

Pro Forma Operating Statement

|

|

|

|

|

|

|

|

|

|

|

|

|

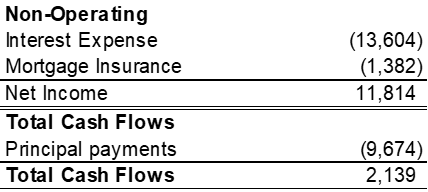

I have about $393,000 remaining on the mortgage which I am lucky enough to carry a 3.5% interest rate fixed for 30 years. After paying interest, mortgage insurance, and principal payments I’m left with just under $12,000 net income and $2,200 of cash flows.

|

|

|

|

|

Debt service and cash flows

|

|

|

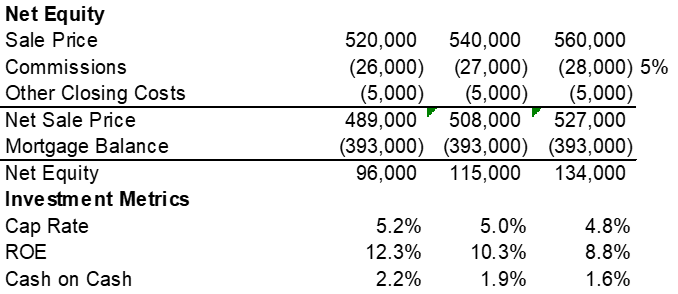

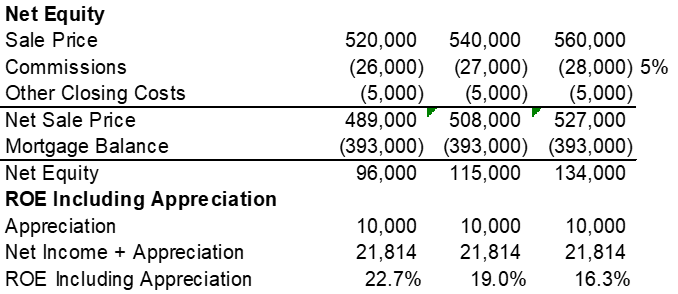

I believe the house is worth approximately $540,000. If I sold the home at that price, I would net approximately $115,000 before capital gains taxes and depreciation recapture. I’m ignoring capital gains taxes because I’m slightly in the red on the property value.

|

|

|

|

|

Equity and return metrics

|

|

|

The net operating income of $26,800 divided by the $540,000 purchase price equals a cap rate of 5.0%. That’s not bad, especially considering I’m allowing for a healthy $6,500 annually in maintenance and capex. That number is heavy for a 1,340 square foot house, but I’ve been crushed with unexpected maintenance over my 4 years of ownership. The high cost of maintenance is the primary reason I want to sell. It was built in 1971 and was not well maintained prior to my ownership. Since buying in 2022 I’ve done an emergency sewer patch repair ($4,300), repaired a gas leak ($1,000) replaced the water heater ($750), replaced pool light ($800), replaced the pool heater ($3,600), re-surfaced the pool and replaced the pump, filter, and control panel ($23,000), replaced garage door motor ($1,500). And there is more to come! The cooling system is way past it’s useful life ($7,000), the pool decking needs to be resurfaced ($5,000). It could use an exterior paint job ($4,000). Damn! I am so tired of the maintenance.

|

|

|

|

|

The decision boils down to this. I could pull out $115,000 by selling the house. By selling the house I am relinquishing $11,646 of net income (10.0%) PLUS future home price appreciation. If we assume the home appreciates by $10,000 (very conservative less than 2%) my return is boosted tremendously to 19% annually of leverage.

|

|

|

|

|

Levered returns look juicy

|

|

|

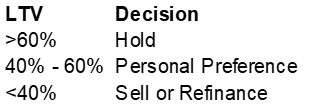

Only one number ultimately matters in a buy vs. sell decision: Loan to Value (“LTV”). The principal balance of the loan ($393,000) divided by the value of the house ($540,000) equals a 73% loan to value. The high loan to value gives me tremendous leverage to benefit from asset price appreciation or inflation. A 10% inflation in the home price over 5 years ($540,000 * 10% = $54,000 appreciation) would result in a 47% increase in my equity value because of leverage ($54,000 / $115,000 net equity).

Levered appreciation is the golden snitch of real estate investing. The monthly cash flows from single family rentals are like throwing the quaffle through the goal for 10 points. The cash flows ultimately prove meaningless compared to the long term principal paydown and price appreciation akin to catching the golden snitch for 150 points.

All this analysis can be boiled down to this table:

|

|

|

|

|

Loan to value is all that matters

|

|

|

|

|

While leverage is an incredible tool to build wealth in real estate, it cuts both ways. If the price of the home depreciated 10%, the value of my equity would decrease by the same 47%. The key is to make sure you are able to service the debt no matter what so you are able to ride out the downturn. Because the asset yields 5% (the cap rate) and my interest rate is 3.5%, the cash flows should easily cover the debt service and I will have no problem holding on to the asset through any down turn, such as the soft downturn we are experiencing now.

In the end, the decision is clear. I am going to re-rent the house and keep it for at least another year. As much as I’m tired of spending money maintaining the home and managing a house in a different state, the golden handcuffs of the 3.5% mortgage still have their grip on me. Pray for some modest home price growth in Tempe, AZ!

|

|

|

|

|

|

|

|

|